Best Practices for Implementing Legal Collections Management Software

6 min read

Most banks and NBFCs that invest in legal collections management software implementation get the buying decision right and the rollout wrong. The platform sits configured to defaults, half the team keeps working from Excel, and external counsel never logs in.

The best practices for implementing legal collections management software are to map your existing recovery workflows before configuring anything, carefully clean and migrate borrower data, build RBI and SARFAESI compliance into the system from day one, and drive adoption through role-based training rather than a single launch-day demo. Implementation, not the software, decides the return.

That gap between a capable tool and a recovery process people actually use is where most of the value leaks out. Here is how to close it.

Buying legal collections management software is the easy part. The hard part is getting a busy legal and recovery function to change how it works every single day, and that is exactly where rollouts stumble.

A platform that gets configured once and never adopted is an expensive shelf ornament. It happens more often than vendors admit. Officers keep using old trackers, managers lose visibility, and the promised efficiency never shows up in the numbers. The cause is rarely the technology. It is a rollout that treated go-live as the finish line rather than the starting line.

Done well, implementation protects your recovery rate, your regulatory standing, and your team's trust in the system. A clean rollout means cases stop slipping through cracks, notices go out on time, and your officers reach for the platform first thing each morning. Teams that plan adoption deliberately tend to reach full utilization in weeks rather than quarters.

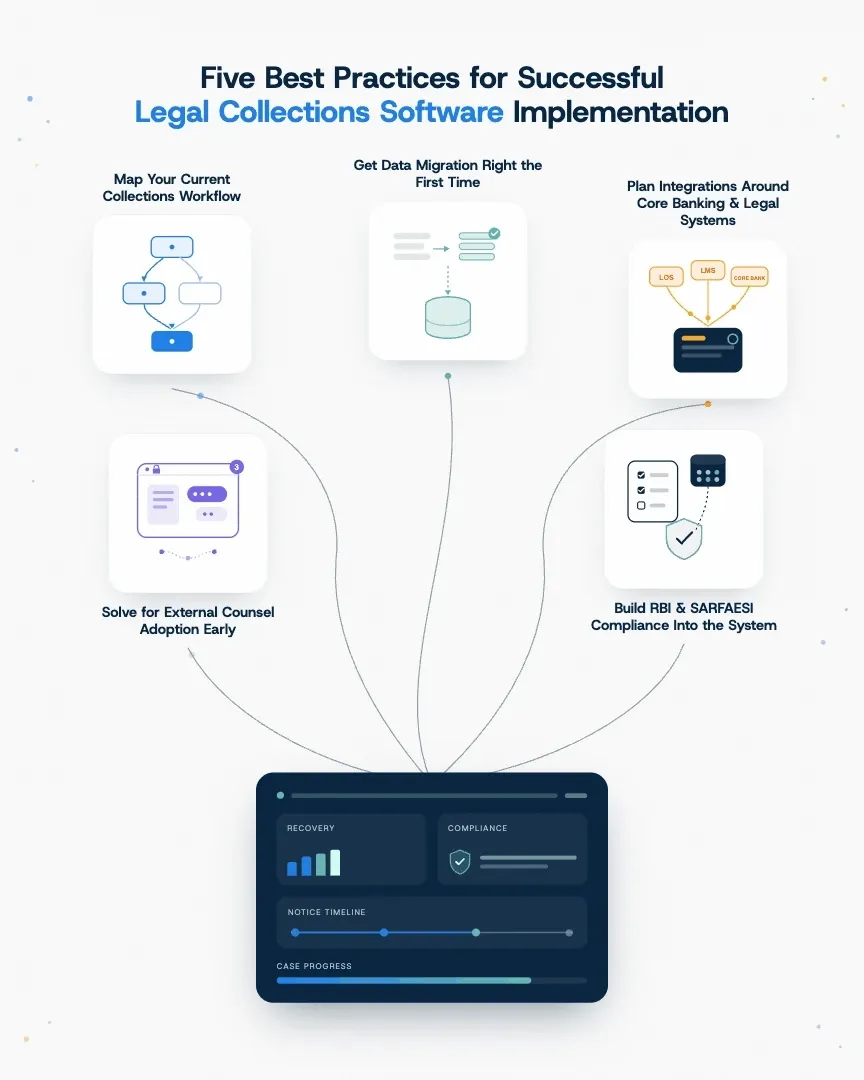

When a borrower account crosses the delinquency threshold, your legal team needs the full account history: demand notices sent, borrower responses, payment conduct, and DPD classification. In most BFSI organizations, that handoff happens over email. Map it before you configure anything.

List every notice your team handles: Section 13(2) SARFAESI demands, Section 138 dishonor notices, loan recall notices, and arbitration invocations. Record the statutory response window for each. Your SARFAESI workflow automation depends on this catalog being complete before setup.

Duplicate borrower records, stale contact details, and half-closed cases will follow you into the new system unless you scrub them first. Dedicate time to deduplicating and validating records before migration, not after. A smaller set of clean data beats a large set of unreliable data every time.

For a few weeks, run the new platform alongside your existing process on a subset of live cases. This surfaces gaps while the old system is still a safety net, so a missed field or a broken notification never costs you a real recovery action or a compliance deadline.

Configure the platform so that SARFAESI notice periods, demand notice timelines, and statutory deadlines automatically trigger with built-in reminders. Every action should leave an audit trail behind it. When a regulator or an internal auditor asks who did what and when, the answer should be one click away, not a week of digging through email.

Compliance data starts upstream. Integrate the collections platform with your loan origination system, loan management system, and core banking so account status, outstanding balances, and borrower details flow in automatically. Manual re-entry is slow, and it is where errors and compliance gaps quietly creep in.

A recovery officer, a legal manager, and a compliance head each lean on the platform in different ways, so training each group on the workflows they touch every day beats a feature tour of the whole product. Role-based training sticks because it answers the only question a busy user cares about: how it makes today easier than yesterday.

Keep your eye on login and usage rates before anything else, because they tell you whether adoption is real, then layer in recovery cycle time, the share of notices issued on schedule, and your resolution rate. When rising usage and shorter cycle times coincide, you have the clearest sign that the rollout is paying for itself.

Rolling out to every external advocate across every jurisdiction at once guarantees resistance. Pick one region or case type (Section 138 matters in a single state works well) and run a focused pilot before scaling.

External counsel are not on your payroll. Limit their access to assigned cases by using mobile-friendly interfaces and keeping mandatory fields to a minimum. Give advocates clear value (hearing updates, access to documents) that makes logging in worthwhile.

The banks and NBFCs that get legal collections technology right treat implementation as a process redesign with a software component, not the other way around. Your rollout sequence, from workflow mapping through counsel adoption, determines whether the platform becomes the operating system for legal recovery or another tab your team ignores.

A platform that mirrors the workflow your team already runs, sits on clean data, enforces compliance on its own, and earns a daily place in everyone's routine will lift recovery rates and shrink regulatory exposure. In contrast, one left idle after launch will manage neither. Treat the rollout itself as the real investment, and let the technology follow.

Most BFSI teams achieve a working go-live within 6 to 12 weeks, depending on data volume and integration complexity. Configuration and data cleanup take the most time. Adoption often extends past go-live, so plan for several more weeks of role-based training and support before the platform reaches full daily use across your recovery and legal teams.

Low user adoption, not the technology. When a platform is configured generically, and teams are trained only once, recovery officers drift back to old spreadsheets and trackers. Mapping the software to your real workflow and training people for their roles are the two practices that prevent this and protect your return on investment.

Build compliance into the workflow rather than treating it as a manual step. Configure statutory notice periods, demand notice timelines, and SARFAESI deadlines to trigger automatically with reminders, and make sure every action leaves an audit trail. Integrate with your loan and core banking systems so that account data stays accurate, up to date, and fully traceable for any audit.

Loan management system for account data, debt management system for portfolio sync, and India Post API for statutory notice dispatch. eCourt API and payment gateways can follow in a second phase.

No. Clean and deduplicate borrower and case records first, then migrate in a controlled way. Running the new platform in parallel with your existing process on a subset of live cases for a few weeks surfaces gaps safely, before you fully cut over and start relying on the system for active recovery and compliance actions.

Dive deep into Provakil's numerous blog posts & discover how legal tech can streamline your litigation, contracts, IP, and notice management processes.