How to Choose Debt Recovery Management Software for Small Finance Banks and NBFCs

8 min read

The gross NPA ratio for scheduled commercial banks hit 2.15% in September 2025, a historic low. But that headline number masks a split. Small finance banks carry disproportionate stress in their retail portfolios, with unsecured loans making up 51.9% of total bad loans in the SFB segment, according to the RBI's Financial Stability Report.

NBFC-microfinance institutions saw their GNPA ratio jump from 2.0% to 4.1% in a single year through March 2025. For legal teams at these institutions, the recovery workload is growing while the teams themselves remain small.

Choosing the right debt recovery management software in this environment requires a different set of questions than what a top-ten private bank would ask.

SFBs and smaller NBFCs deal with high case volumes at low ticket sizes, limited in-house legal bandwidth, and statutory constraints that narrow the recovery routes available for certain accounts. This piece covers what to evaluate and in what order.

SFBs hold banking licenses, but their loan books look nothing like those of commercial banks. Small-ticket lending across thousands of borrowers in dispersed geographies means delinquency is high-volume and low-value per account, so chasing each defaulter through a separate manual process quietly eats whatever margin the loan was supposed to earn.

Add a mix of secured and unsecured exposure, a lean in-house legal team that is often a handful of people, and the heavier RBI scrutiny that smaller regulated entities now face, and the conclusion writes itself. The software that suits a large bank's call-center floor will leave you exposed exactly where recovery gets expensive and where regulators look hardest.

Both institution types share a common problem: the legal recovery function operates with a handful of managers overseeing dozens of external advocates, and a single missed filing deadline or untracked hearing date can stall recovery on an entire batch of cases.

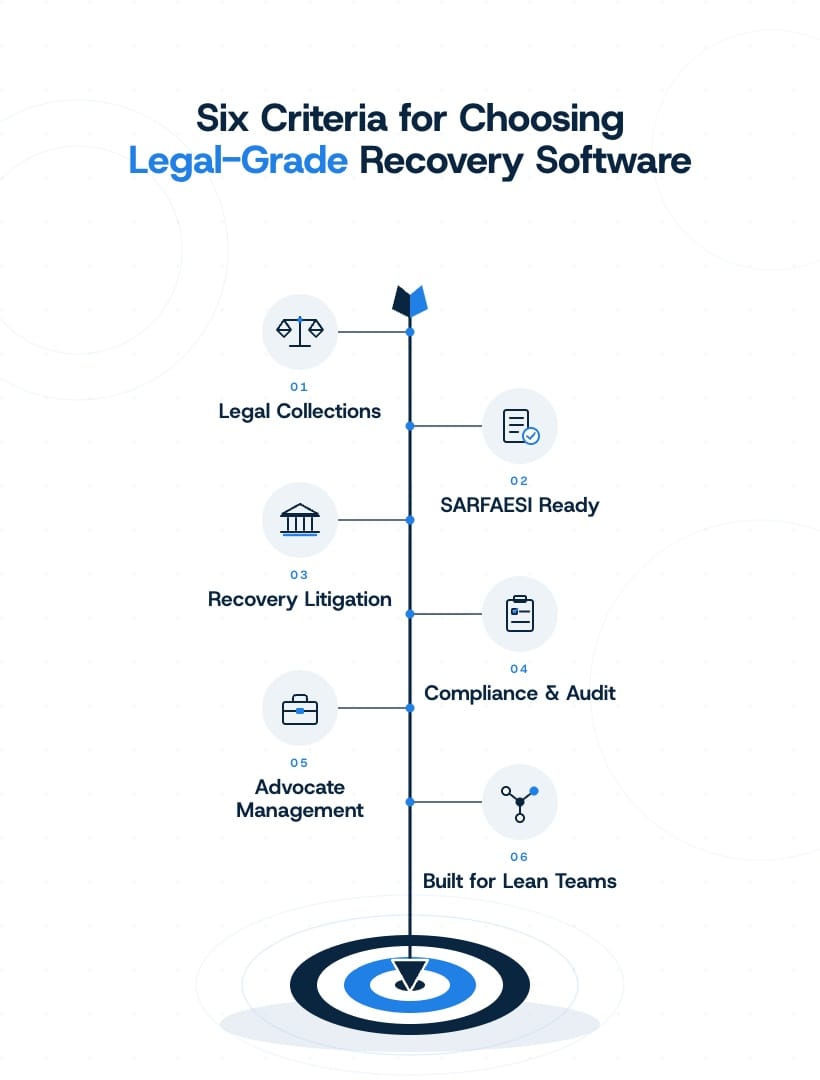

The Indian collections technology market has built strong capabilities around AI calling, digital dunning, and field agent tracking. Those tools serve the operations team. The legal recovery layer is a separate evaluation, and the legal head or collections legal manager should own it.

A purpose-built legal collections management platform handles the work that begins once a loan enters the legal track: generating and dispatching statutory notices, enforcing workflow timelines for each recovery statute, tracking litigation across forums, and managing external advocates. Evaluate the following capabilities within that layer.

Plenty of vendors will show you a slick dialer, an auto-reminder engine, and a field-agent app, then go quiet when you ask what happens after soft recovery fails. That silence is the whole problem, because the accounts that survive tele-calling are precisely the ones that need a clean handoff into legal recovery rather than a dead end.

Look for a platform that treats legal collections management as a continuous lifecycle, where a stalled account flows automatically from reminders to notice issuance and, if needed, to litigation, carrying its full history so nothing is re-keyed and no deadline is lost during the transfer between teams.

For secured lending, the speed and accuracy of your notice machinery often decides how much you actually recover. A capable platform should generate, dispatch, and track demand notices and possession notices in bulk while respecting the statutory SARFAESI timelines governing each stage, so a 60-day clock or a symbolic possession window never slips because someone forgot to diarize it.

The same logic applies across your unsecured book, where structured Loan Recovery Management keeps every legal notice, its mode of dispatch, acknowledgment, and response logged against the correct account.

Volume is the quiet differentiator here, since issuing a few hundred notices a month by hand is feasible and issuing several thousand defensibly is not, and that difference is the line between a tool that scales with your book and one you outgrow within two quarters.

When recovery moves to a Debt Recovery Tribunal, a Lok Adalat, or a civil suit, the work fragments across forums, dates, and advocates scattered over a wide map, which is exactly where small legal teams start dropping hearings and missing orders.

A platform with real Litigation Management pulls every matter into a single view, tracking case status, hearing dates, cause list updates, and next actions, so your team walks into each week knowing what is listed where and what each matter needs, rather than reconstructing it from a panel advocate's email at the last minute.

Recovery that wins money but cannot be defended on paper is a liability waiting to surface in an inspection, and smaller regulated entities are feeling that pressure more keenly than ever.

The right system should log every action automatically, capturing who issued which notice and when, how each borrower was contacted, and what each recovery agent did in the field, so that compliance with the fair-practices code and the recovery-agent norms is evidenced by the record rather than asserted after the fact.

SFBs and small NBFCs send most courtroom work to empanelled external advocates. Recovery outcomes depend on how you allocate, track, and evaluate that panel.

The platform should assign cases based on advocate expertise, geography, and current workload. Stage-based billing, where you see the cost at each litigation stage per case, gives you a cost-control lever that compounds across hundreds of active matters. Track closure rates and recovery amounts by advocate to make retention decisions based on performance data rather than institutional habit.

A recovery platform that requires its own data entry will quietly add headcount you cannot justify, so integration is not a nice-to-have but a precondition.

The software should sync borrower, loan, and delinquency data from your loan origination and loan management systems through clean APIs, so an account flips into recovery the moment it qualifies, without anyone retyping a single field.

The question to put to every vendor is plain: will this run on the people I already have as my book doubles, or will it demand more of them with every thousand new accounts?

It is tempting to treat this as a procurement exercise in which the cheapest dialer that ticks a few boxes wins, but for a small finance bank or an NBFC, the recovery platform is closer to a balance-sheet decision than a software one.

When you weigh a platform against all six questions together rather than one at a time, the field narrows fast, because only a handful of systems genuinely hold the full lifecycle, stay defensible under an RBI lens, and run on the lean team you already have rather than the one a vendor assumes you can hire.

The right choice does not merely speed up your existing process; it changes how much you recover and how confidently you can answer for every rupee you chase, which is precisely the difference a smaller lender feels most.

Provakil brings legal collections, SARFAESI notices, DRT and recovery litigation, and a complete audit trail onto one connected platform built for exactly that reality.

It is a platform that manages the full delinquent-account lifecycle for a non-banking financial company, from soft collections and reminders through legal notices, SARFAESI action, and recovery litigation. Unlike a tele-calling dialer, it keeps collections and legal recovery in a single record, automates statutory timelines and audit trails, and integrates with loan systems so accounts move into recovery without manual re-entry.

Small NBFCs and SFBs run high-volume, small-ticket books across dispersed regions with lean legal teams, so they need automation that handles an account end-to-end rather than software that only handles early-stage calling. The priorities shift toward bulk notice issuance, scalable litigation tracking, and built-in compliance evidence, because there is no large in-house team to handle the legal stages by hand.

Manual notice generation for a few thousand delinquent accounts takes days per batch: pulling borrower data, populating templates, handling jurisdiction-specific variations, dispatching through India Post, and tracking delivery. Automation compresses this to hours. The platform imports data from the LMS, segments accounts by notice type, applies the appropriate statutory template, dispatches in bulk, and tracks delivery with proof of delivery.

Capable platforms do. They generate and dispatch demand and possession notices in bulk, track the statutory SARFAESI timelines for each stage, and log acknowledgments and responses against every account. This keeps secured recovery moving on schedule and produces the documented trail a lender needs if any step of the enforcement process is later questioned.

Yes, by making compliance a matter of record rather than recollection. It automatically timestamps every notice, contact, and field action, evidencing adherence to the fair-practices code and recovery-agent norms. When an inspection or a borrower dispute arises, a complete activity trail allows a lender to quickly demonstrate compliant conduct rather than reconstruct it from scattered emails and spreadsheets.

Dive deep into Provakil's numerous blog posts & discover how legal tech can streamline your litigation, contracts, IP, and notice management processes.